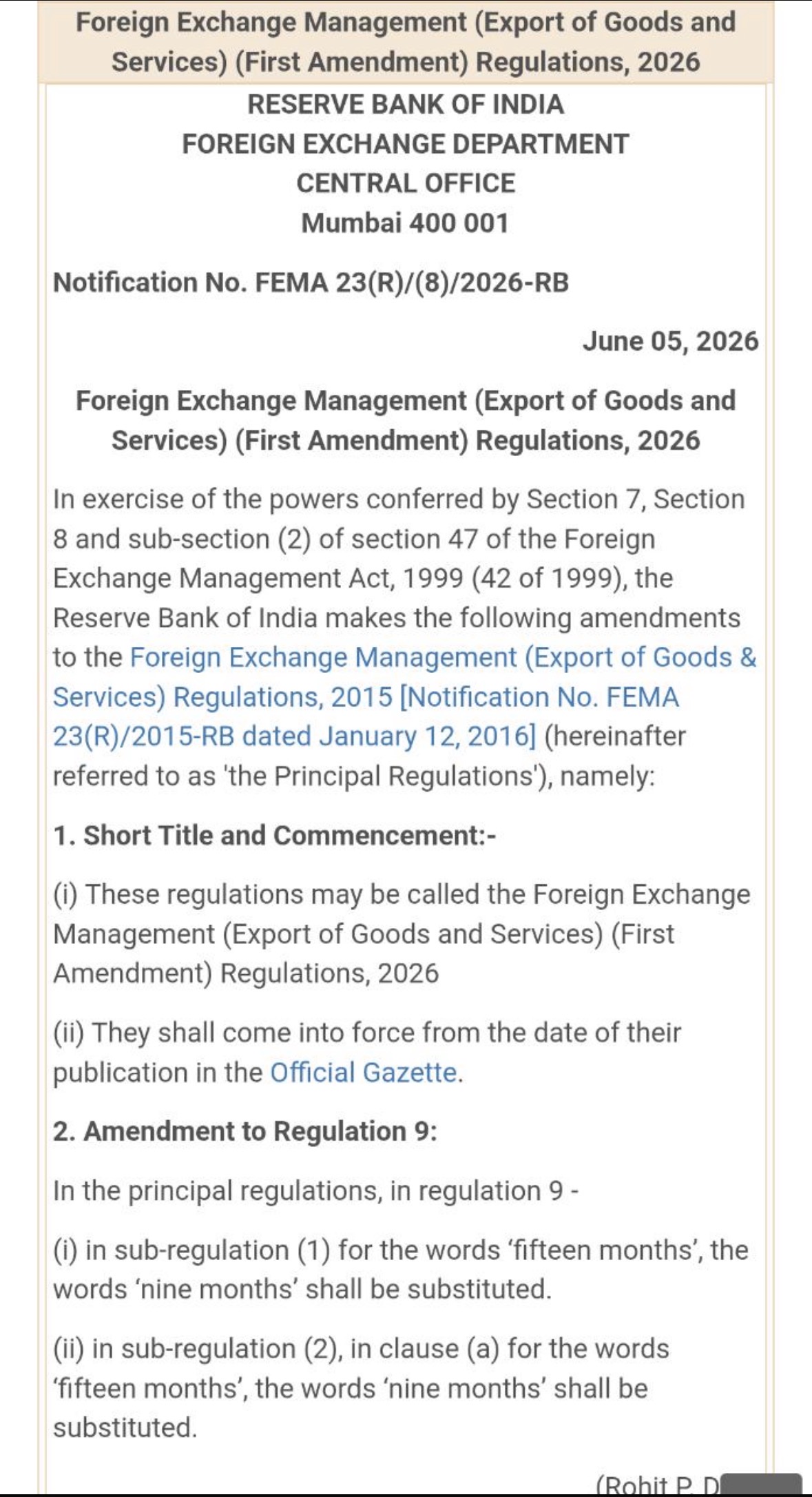

If you are an exporter in India, it is time to check your calendar and audit your receivables cycle. The Reserve Bank of India (RBI) has just announced a major policy shift, restoring the mandatory time limit for realizing and repatriating export proceeds back to 9 months. Earlier time limit was 15 months which is now reduced to 9 months effective from 5th June 2026. This return to the 9-month rule applies uniformly across all categories, including standard Domestic Tariff Area (DTA) units, Special Economic Zones (SEZs), and 100% Export Oriented Units (EOUs).

If you have been granting extended credit terms (say, 12 months) to capture foreign market share, you can no longer legally do so without explicit, case-by-case bank approvals. You must realign your standard commercial terms to ensure payment drops well before the 9-month mark. |

What if 9 Month deadline is jumped :

If the 9-month deadline is "jumped" (meaning you have passed day 270 from the date of shipment and the funds haven't hit your account), the clock doesn't just stop—the system automatically pushes your transaction into a red-flagged state. -

Authorized Dealer (AD) bank will refuse to process or handle any new export shipping documents unless you provide a 100% advance payment or an irrevocable Letter of Credit from your future buyers

- If you exported under a Letter of Undertaking (LUT) without paying integrated tax, you are legally required to pay the applicable GST on that transaction out of pocket, along with accumulated interest, if the money is not received within the time limit.

- Any tax refunds or duty drawbacks you already pocketed from the government for that specific shipment must be refunded back to the authorities until the foreign remittance is successfully cleared.

-

Under Section 13 of FEMA, non-repatriation of foreign funds is a civil offense. If the regulatory authorities find that you didn't take active, reasonable steps to recover the money, they can impose a penalty of up to three times the amount of the un-realized export proceeds.

|

Conclusion:

It's time to update your automated tracking systems, tighten up your invoice follow-ups, and ensure your finance teams are strictly aligned with the restored 9-month rule. Disclaimer:

The above information/amendment/provision is to be used for ready reference only and not to be construed as legal/Professional advice. |